by Berta Calders | Oct 11, 2019 | Coworking, Impact

Maria 01 is a Finnish non-profit combination of an entrepreneurial community, a selective campus for tech teams and a technology builders club. Owned in part by the same owners as the Nordic’s biggest startup conference, Slush (25.000 attendees every year), Maria 01...

by Berta Calders | Jun 21, 2019 | Business, Coworking Europe

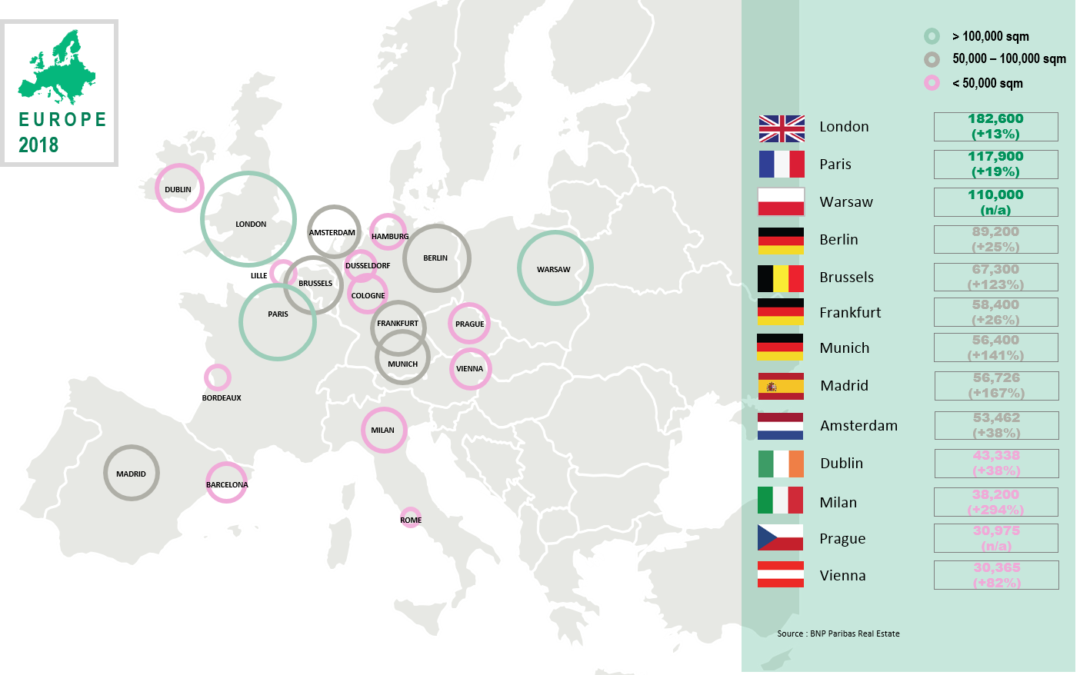

Coworking has be around for more than a decade in Europe. Nowadays, coworking reaches out to every corner of the continent. BNP Paribas Real Estate released a study spotting the new upcoming coworking hotspots in Europe and what drives the growth. We interviewed...

by Jean-Yves Huwart | Aug 13, 2018 | Business, Coworking Europe, Data, Design

Founded in 1999, The Instant Group rethinks workspace on behalf of its clients, injecting flexibility, reducing cost and driving enterprise performance. Instant places more than 7.000 companies a year in flexible workspace such as serviced, managed or coworking...

by yvandeuren | Feb 19, 2018 | Business

Eduardo Salsamendi is involved in the industry of flexible workspace since 1990. That year, he founded his first business center Klammer located in Northern Spain. In 2008, Eduardo Salsamendi founded the European Confederation of Business Centers Associations...

by Jean-Yves Huwart | Jun 23, 2017 | Business, Coworking Europe

Hector Kolonas is the founder of Included.co, an online platform organising group purchases for a network of over 200 coworking communities in the world. The service helps the spaces to buy supplies and services at a discounted price, thanks to the generated volumes....